RealVantage's COVID-19 Viewpoints and Strategies

The COVID-19 pandemic has brought the world to its knees and into uncharted territory on many fronts.

Table of Contents

- Coronavirus Situation Stock Take

a. Global Financial Market Correction: Fastest Crash On Record

b. Credit Markets: Flight to Quality, But Still In Business

c. Impact On The Real Economy: Last One Out Loses The Most - Economic Outlook and Investment Strategy

a. Going Defensive, Avoid Hero Calls - RealVantage’s Real Estate Investment Strategies

b. Core strategy is our primary strategy

c. Thematic approach

d. Opportunistically Opportunistic

The COVID-19 pandemic has brought the world to its knees and into uncharted territory on many fronts. Staring into an abyss of uncertainties, investors who have not been paralysed into inaction are either nursing their wounds while realising losses or formulating and recalibrating investment strategies to capitalise on opportunities engendered by these truly extraordinary times. We are in the latter camp.

This article does not constitute financial or investment advice. Rather, we draw upon our past experiences investing through boom-bust cycles, while taking into account the unique nature of the current challenges to share our perspectives on real estate investment. We hope these views will provide a useful reference to readers as they navigate through these challenging times. To lay out the context guiding our investment strategies, we (1) take stock of the health crisis situation, (2) make inferences on the financial and credit markets as well as real economic impact, and (3) project the implications onto a recovery profile.

Coronavirus Situation Stock Take

The Flattening Curve – which plots the total number of confirmed cases against time elapsed – is an important chart that gives a picture of where the virus situation is. The idea for situation control is to impose protective measures and manage the number of virus cases such that it does not exceed the healthcare capacity threshold while the occurrence of new cases eventually tapers off to zero (levelling of the graph).

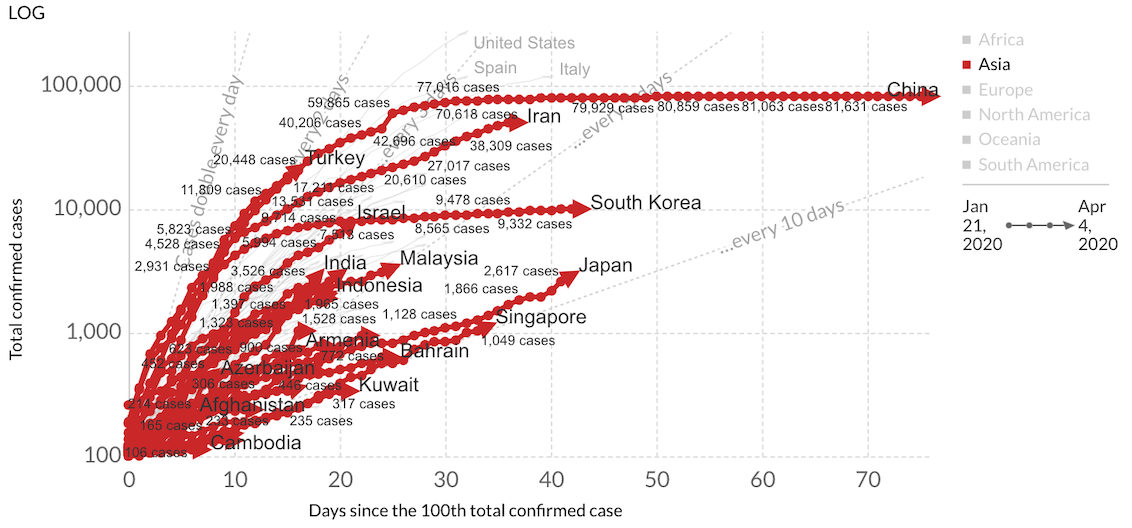

Figure 1: Asia Coronavirus Flattening Curve

Based on the latest data, Asia has been a reassuring picture of stabilisation (Figure 1), with most countries on the path to containment. Certainly, Asia’s experience with the SARS outbreak in 2003 would have been valuable in the current episode. Notably, China announced that the lockdown on Wuhan – ground zero of the pandemic – will be lifted from 8th April, marking a significant milestone in the battle against the outbreak.

Elsewhere in Asia, progress has been encouraging with most countries looking like they are past or near an inflexion point on the curve. The risks of second waves and reversal of data trend remain however, given news of suspected under-reporting, mass gatherings and more widespread testing.

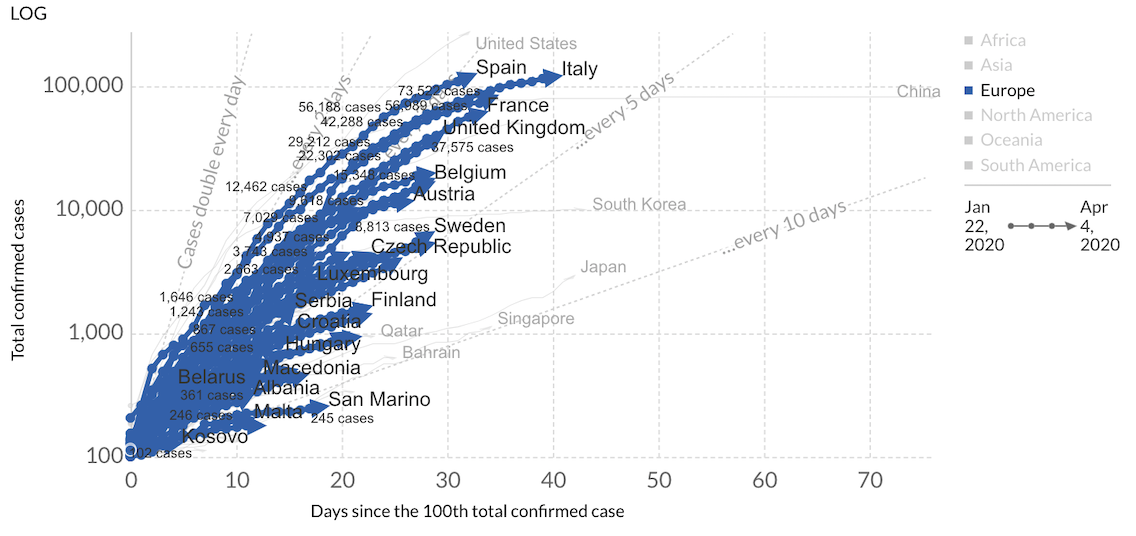

Figure 2: Europe Coronavirus Flattening Curve

Europe remains some way from getting a firm handle on the situation. In early-March, the European Centre for Disease Prevention and Control (EDCD) warned that the risk of European healthcare systems getting overwhelmed is high if the outbreak remained on the same trajectory. Comfortingly, many EU member states have taken aggressive containment measures and the situation has evolved encouragingly since, with most countries leaning more towards the right side of the flattening curve by end-March (Figure 2). Given the coordinated government response, we are optimistic of European countries reaching more pronounced inflexion points in the near future.

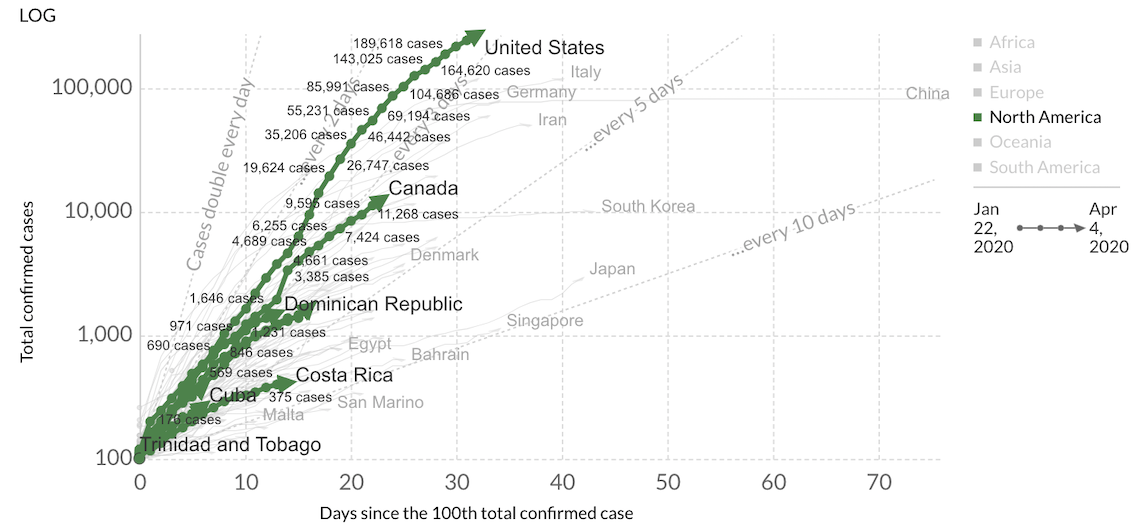

Figure 3: North America Coronavirus Flattening Curve

As of the time of this writing - the virus situation in the US remains deeply troubling (Figure 3). The country now accounts for the highest number of confirmed incidences globally and remains on a dangerous trajectory where cases are doubling every 2 to 3 days. Circumstances in the New York tri-state and neighbouring areas are particularly acute, with more than half of the US’s confirmed cases concentrated in this region.

Further, there are 3 other virus hot zones building up within US – Miami, New Orleans and Houston; Each one with potentially as large an impact as in New York. Yet a coordinated national plan to mobilise resources where they are most needed and which the patchwork of politically polarised state governments can act on remains missing. In the absence of strong federal government direction, governors have gone their own ways, with most adopting stringent measures (thankfully) while others continue dithering. The consequence of such divides will surely be felt in the coming months.

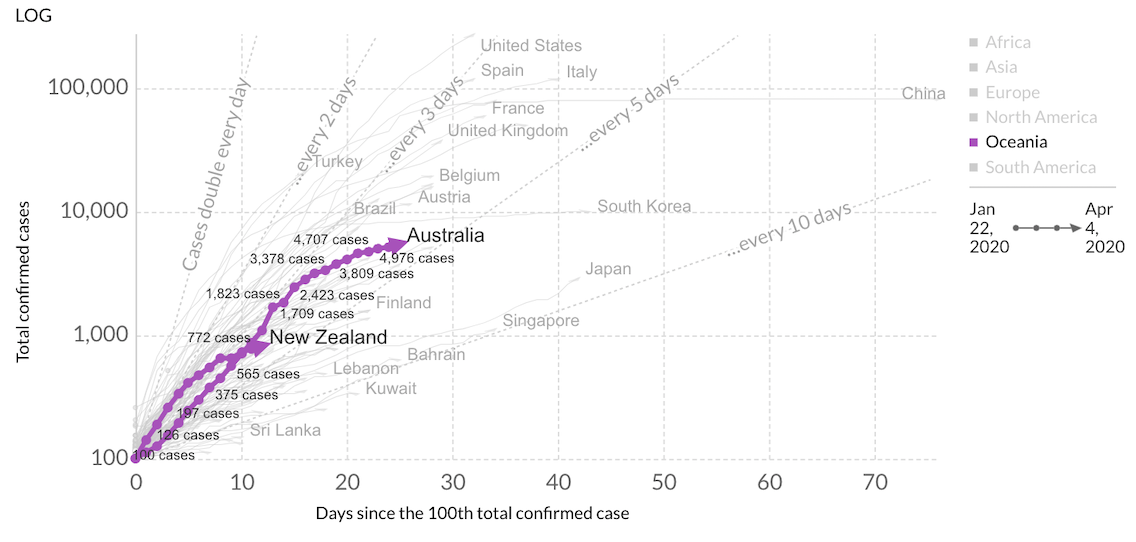

Figure 4: Oceania Coronavirus Flattening Curve

Australia remains on a steep growth trajectory of doubling cases every four days or so (Figure 4). But there are reasons for optimism, not least because the number of cases remain relatively small. Decisive government response and rigorous testing have yielded early and modest results. Though not sustained yet, verifiable signs of flattening the curve have emerged.

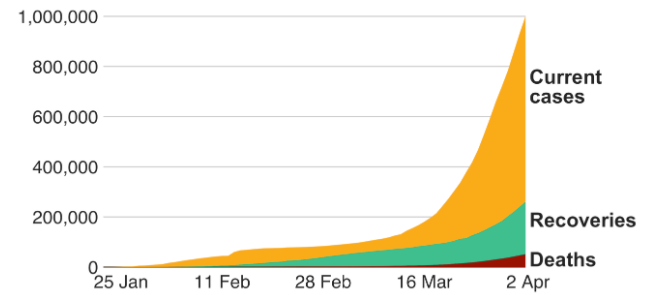

Figure 5: Global Viewpoint of the Coronavirus

From a global viewpoint, it looks like we are some distance away from the point when the overall virus situation gets under control (Figure 5). Given the uncertainties and permutation of variables in play, it would be impractical to put a time estimate on the health crisis with any degree of confidence, not least because it is outside of our domain knowledge. Current models by healthcare experts predict the peak would occur around July and the outbreak would last until early fall. If it is anything to go by, a “long stop date” could likely be set as the estimated time required until a vaccine comes along, which experts say will take 12 – 18 months from now.

Read also: Implications of COVID-19 Aftermath on Real Estate Sectors

Sign Up at RealVantageGlobal Financial Market Correction: Fastest Crash On Record

It was not until past mid-February before financial markets recognised the severity that the impact of the coronavirus pandemic has on the global economy. After reaching their respective record highs earlier during the month, major stock indices across the world plunged precipitously on 20th February. In the one month thenceforth, indices fell about a third peak-to-trough.

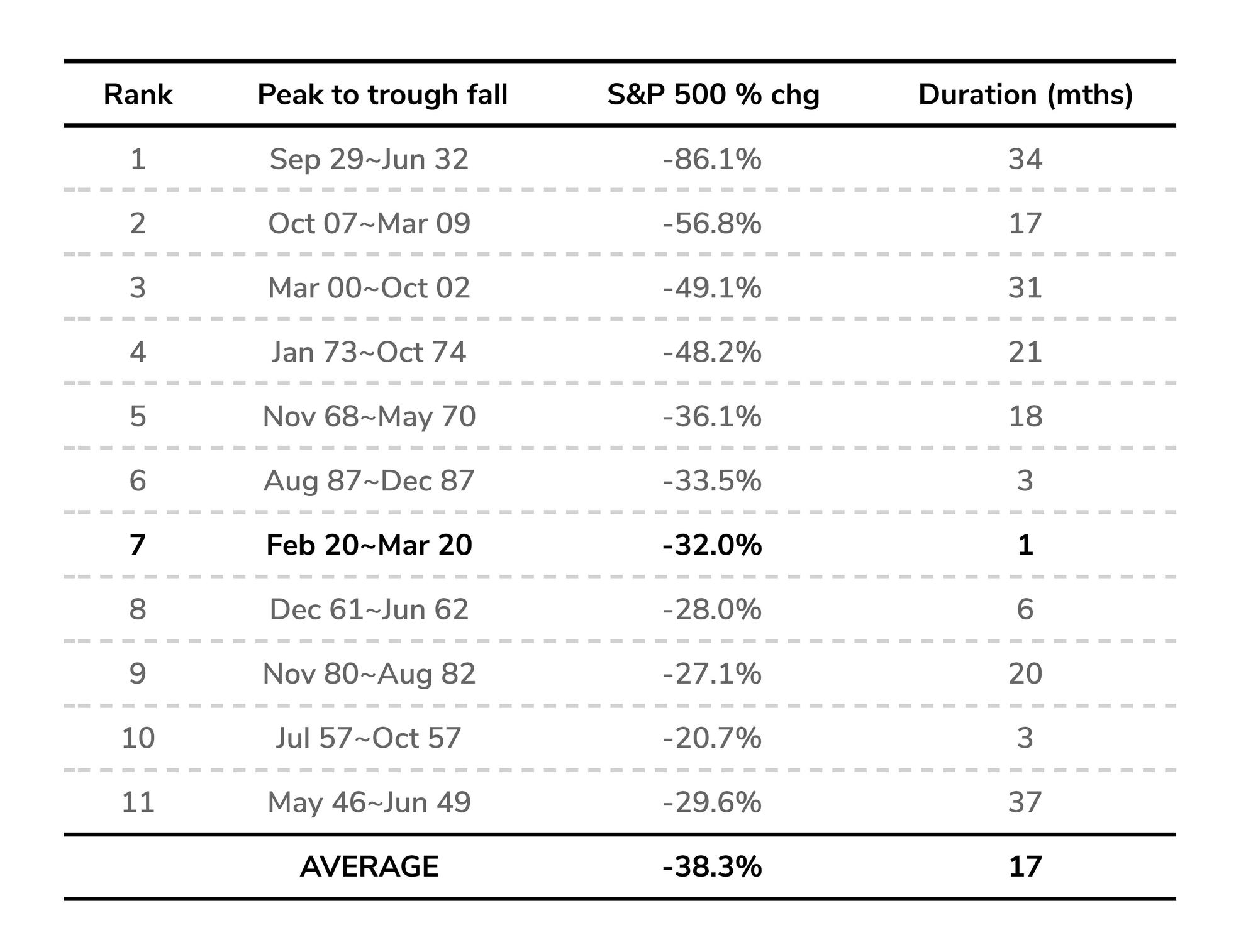

Figure 6: Historical Corrections of the S&P 500 Index

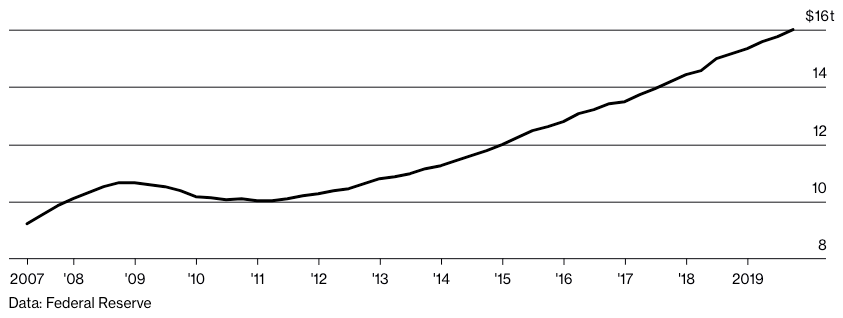

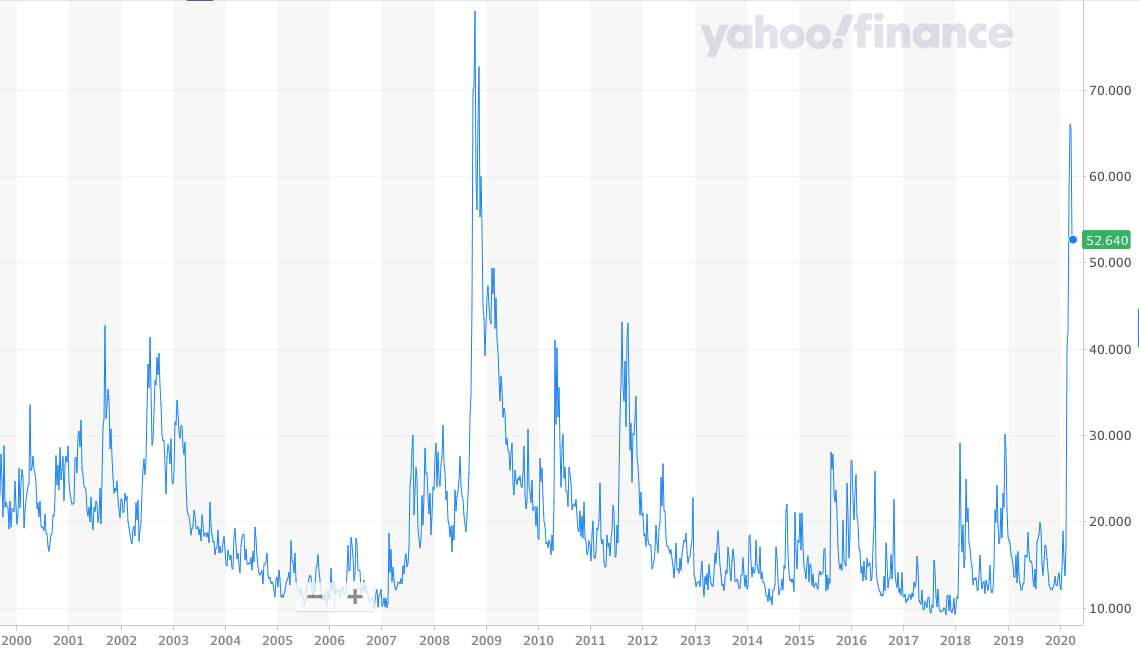

In perspective, while the magnitude of the market crash (so far) is smaller than in previous episodes, the pace of decline is unprecedented (Figure 6). Importantly, the coronavirus exposed the vulnerability of heavily leveraged businesses (Figure 7) that binged on over a decade of low cost debt in the GFC aftermath. The “fear index”, otherwise known as VIX Index – a widely-used proxy for global risk aversion – spiked to levels only last seen during the GFC (Figure 8).

Figure 7: Mounting Outstanding US Business Debt

Figure 8: VIX Index Levels

Read also: Market Selection in Real Estate - RealVantage’s Approach

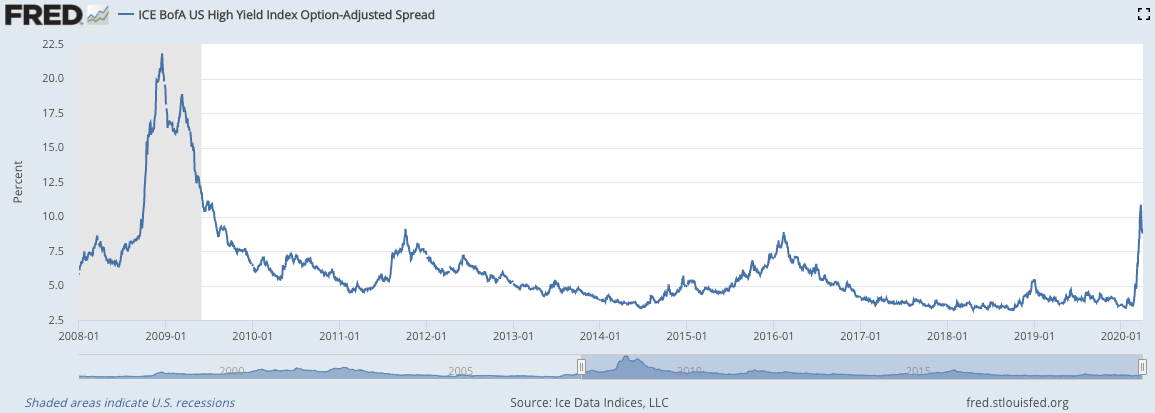

Credit Markets: Flight to Quality, But Still In Business

Credit markets have been spooked by the ongoing levels of volatility and uncertainty. While our channel checks reveal that banks remain eager to do business, credit availability and pricing across the market spectrum have predictably reacted with the usual knee-jerk response amid this risk-off environment. Credit spreads across the risk spectrum – from investment grade to junk bonds – widened by about 300% against risk-free Treasury rates between 20 Feb and 23 Mar before reclaiming some modest grounds (Figure 9).

Despite the sharp spike, we are in a very different situation as compared with the GFC episode when the wheels came off the credit markets because nobody knew how deep the financial contagion ran.

Figure 9 : Spreads of Investment Grade (Top) and Below Investment Grade Bond (Bottom) Indices versus 3-month Treasury

From our interactions with banks, we observe that capital up and down the stack remains at play, but the bias is clearly leaning towards senior debt. Lenders are seeing the opportunity to take on prime clients, especially those capable of taking on higher leverage on certain assets. Abbreviations like NNTB – “No new to bank” – are gaining traction as banks focus on looking after existing customers. Appetite for the subordinated debt market has retreated, particularly from the non-bank segment, mainly to take stock of the market. In a nutshell, the flight to quality has taken root.

Anecdotally, acquisitions by blue-chip investors (the likes of Blackstone, Nuveen, Savills Investment Management, Harrison Street) are still getting funded during this period, notably into sectors that are relatively less susceptible to the virus impact (health care, multi-family and logistics assets). On the other end of the spectrum, a liquidity crunch is forcing Singapore listed Eagle Hospitality Trust –arguably amongst the most at-risk real estate sector – to liquidate assets to raise cash. While lenders are still open for business, they have turned highly discerning over who and what they will lend to, mirroring the flight to quality theme playing out in the fixed income market. We bear this in mind in the strategy section to come.

Read also: What is Dividend Yield?

Read also: An Overview of Investing in REITs in Singapore

Impact On The Real Economy: Last One Out Loses The Most

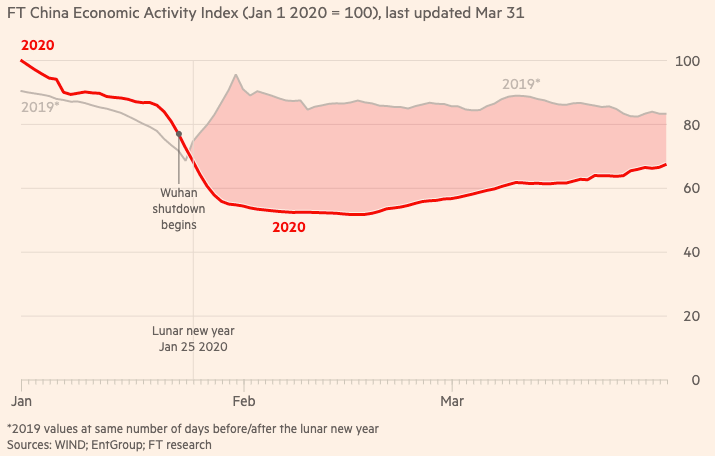

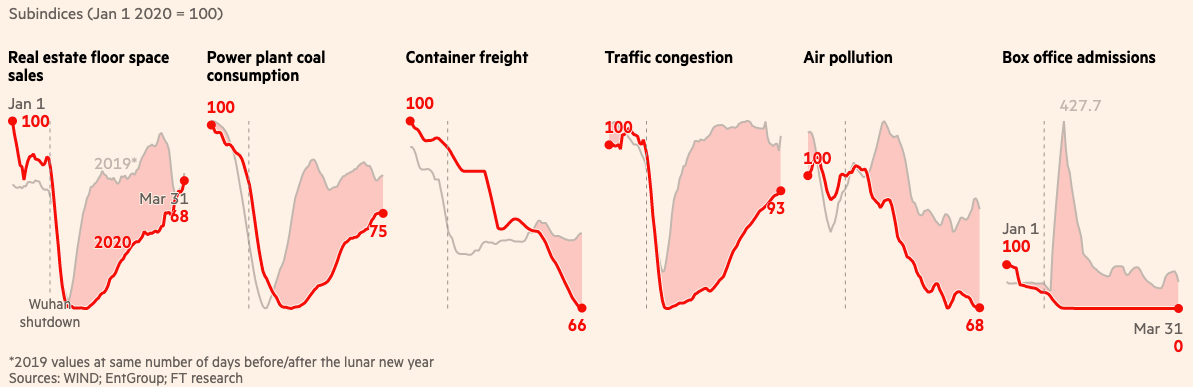

Given that China was ground zero of the COVID-19 outbreak and is the pack leader on the path towards economic normalisation, we look at recent data from China to form some sense of the impact to the real economy. Here, the Financial Times China Economic Activity Index (Figure 10) – which tracks alternative- and industrial-based data series – provides a useful co-incident indicator that is less susceptible to political manipulation.

Figure 10: COVID-19’s Impact On The Chinese Economy

Data shows how economic activity diverged sharply from 2019 levels in the immediate period following the shutdown in Wuhan. After stalling at approximately 35% below the previous year’s levels for much of February when the economy was hardest hit by the lockdown, the gap has closed progressively since then to about 20% below where it should normally be by the end of March as markets cranked back into action. Just earlier this week, China’s official manufacturing purchasing managers index (PMI) bounced back into expansion territory with a reading of 52.0 in March from a record low of 35.7 in February.

The picture is corroborated by the Caixin/Markit PMI, a private survey, which rebounded from 40.3 in February to 50.1 in March. Both data series vindicate Financial Times’ co-incident data trend to some extent.

China’s economy now has to grapple with the reality of dampened global demand for its exports. Thanks to years of structural reforms, China’s economic resilience has improved. Consumption has been the largest contributor to GDP growth for five consecutive years (76.2% in 2018 and an estimated 80% for 2019). Even if external demand falls off by 50% and assuming the government’s stimulus measures lend meaningful support to consumption while spurring an investment-led recovery, the odds of a fast recovery remain viable for China. Note that this is the scenario for an economy that got the virus situation under control within 3 months.

For western economies, the outlook is less sanguine, especially for late actors that will take much longer to subdue the virus outbreak. By the time they emerge from the virus-driven “ice age”, they may very well reset to levels of 70% or less, compared to where they were before the pandemic. Many face the risk of permanent damage to parts of their economies after prolonged hypothermic conditions.

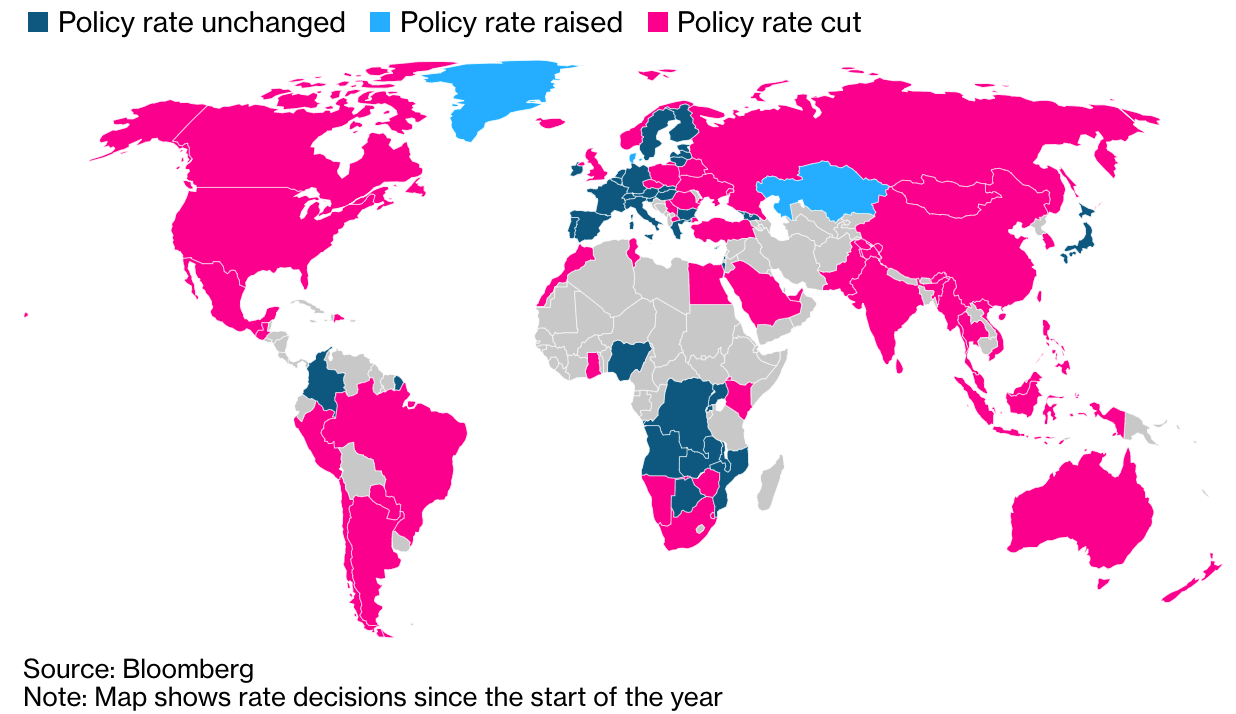

To avert deep economic crises, central banks around the world were quick to slash policy interest rates (Figure 11). Unfortunately, with many countries already in low, if not negative, interest rate territory heading into the virus crisis, there is limited room to manoeuvre and stimulate economic activities. Hampered by limited monetary policy headroom, governments globally have unleashed aggressive fiscal measures, many of which are of epic and never-seen-before proportions. Whether the already announced measures are sufficient to stem the haemorrhage depends very much on how long it would take to get the virus situation under control.

On this point, we draw some comfort from governments posturing a “whatever-it-takes”, “hold-nothing-back” approach although it is implementation rather than simply announcement of policy measures that count. Lastly, we remain wary of potential aftershocks that can come in many shapes and forms – secondary waves of virus cases, widening of geopolitical fractures, social unrests and political repercussions etc. These scenarios are on the risk monitor at RealVantage.

Read also: Selection of Real Estate Co-Investment Platforms (Best Practices & Risk Management)

Read also: Important Considerations when Buying Overseas Properties

Figure 11: Aggressive Monetary Policy Response Worldwide

Economic Outlook and Investment Strategy

As unprecedented (in some ways) as these times are, the bigger picture may not be all that unfamiliar. Notwithstanding differences in the nature and transmission mechanism of the shock, there is much value in drawing on past experiences. As Mark Twain said, “history doesn’t repeat itself but it often rhymes”.

Given the level of uncertainties, the margin of error for any calls on the bottoming of the economy is very high. Yet rather than waffling down a middle-of-the-road non-answer, we would work on the base case that a global recession would be over before the end of the year at best, or last no longer than the 1.5 years experienced during the GFC episode at worst.

- As borne out by China’s and South Korea’s experiences, the virus situation is a direct function of the protective measures implemented. If the shutdowns taken by governments worldwide is anything to go by, we expect flattening curves to level off in the foreseeable future.

- The nature of the shock is more manageable (aforementioned point) compared to the GFC period when uncertainties surrounding the depth and reach of toxic financial contagion practically froze out credit markets (the lifeblood of any economy). In the current episode, credit markets are still functioning, albeit with a huge dose of help from governments.

- The scale, speed and coordinated timing of stimulus packages from governments worldwide are likely to be the game changer. This is very unlike during the GFC when bailout packages faced political resistance (seen by many as Main Street bailing out Wall Street) and were relatively slow to be deployed.

- Given the speed and depth of financial market correction, signs of bargain hunting and some reversal in (equities) investors positioning have already begun. This is an important pre-condition for market stabilisation.

- Last but not least, the possibility of a cure or vaccine remains a possible outcome.

On a counter-intuitive note and despite potential further downsides, we think the costs of inaction now outweigh the opportunity costs for investors to stay completely on the sidelines.

- The best value is to be had when opinions are divided on economic prospects. By the time there is light at the end of the tunnel, asset owners will just hold out. History has taught us that global health emergencies, as dire as the current coronavirus threat seem, are eventually transitory.

- Given the unprecedented liquidity, we expect asset markets (including real estate) to rebound further ahead of economic recovery than is usually the case.

- If the last decade was one characterised by record low interest rate environment, the next lap will be one of ultra-low interest rate, given the swathe of liquidity sloshing around. Virus and recessions aside, we are still getting closer to retirement age. The implications of being out of the market on the retirement nest are substantial.

- Last but not least, defensive real estate investment still offer attractive investment returns through recessionary periods.

Going Defensive, Avoid Hero Calls

Having the benefit of investing through previous cycles, we cannot emphasise enough the importance of adhering to a disciplined, long-term investment approach. In times of extreme market stress such as this, investors might instinctively gravitate towards an opportunistic strategy to zoom in on hugely discounted assets. Adopting such an approach as the go-to strategy might feel like the right thing to do, but history says otherwise.

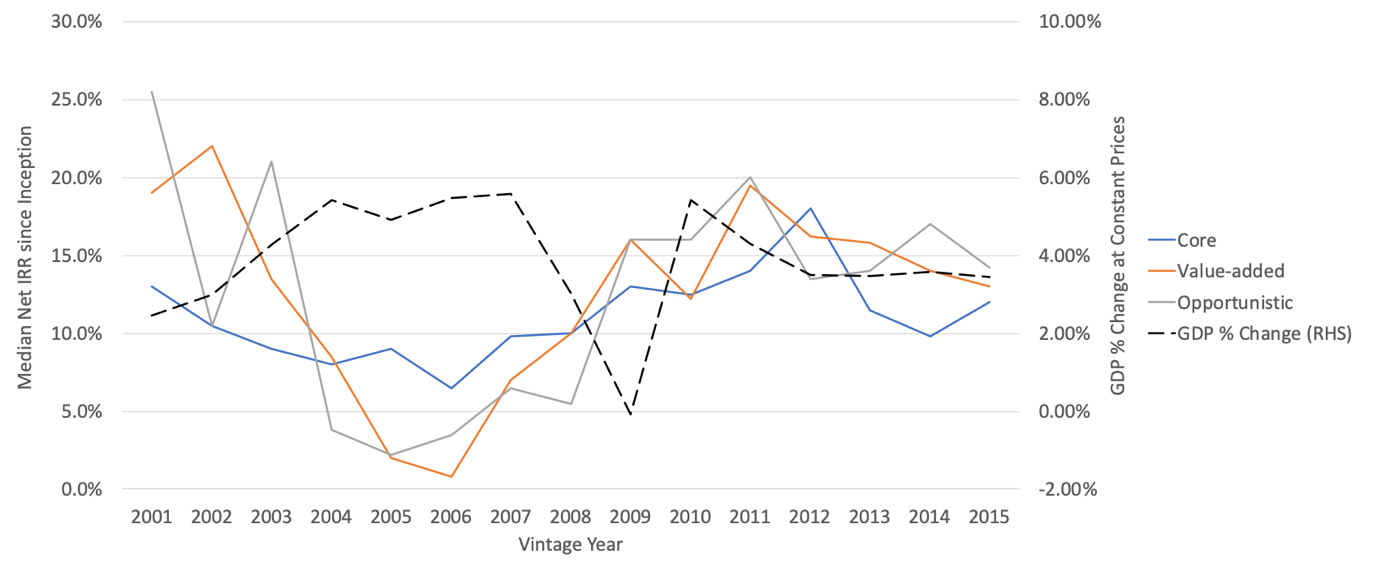

Figure 12 tabulates median IRRs according to the vintage year of funds adopting various investment strategies through the GFC recession. Note that these are sophisticated institutional investors with a typical fund life of 5 to 7 years. A core strategy outperformed value-add and opportunistic strategies on an IRR basis in the early stages of the downturn (we reckon this is where we are at now).

Although median IRRs of value-add and opportunistic strategies were somewhat higher in the late stage of the downturn and immediate recovery leg, the 3.5% – 4% IRR premium hardly compensates investors sufficiently for the additional risks incurred, in our opinion. On a risk-adjusted returns basis, investors remain better off staying defensive with a core strategy while targeting an IRR in the region of 10%.

RealVantage’s Real Estate Investment Strategies

This is what our investment strategies look like in the immediate to near term.

Core strategy is our primary strategy

Target prime locations while staying cautious on fringe locations. The flight to quality is a recurring theme in times like these, as already witnessed in the credit markets. In countries with long lease structures the likes of Australia, Europe and US, assets with existing long leases to strong tenants top our target list. Such leases provide investors with a highly visible income stream to bridge them over this period of uncertainties.

On the other side of the recession, we believe the flush global liquidity would send cap rates ever lower, giving investors of prime locations the added capital appreciation boost. If one thought cap rates in London and Sydney were low before the virus situation exploded, be ready for even lower cap rates in the aftermath of COVID-19. It naturally follows that investors would do well to adopt an investment horizon of at least 4 to 5 years.

Thematic approach

We think that the “rising tide will float all boats” situation is a thing of the past. While beta-oriented investing worked well previously, the coronavirus episode is likely to leave legacies that require a more thematic approach to investing.

Resetting logistics and supply chains – Look for acceleration toward localisation and regionalisation, and moves away from globalised supply chains as firms calibrate away from simply efficiency to supply chain security. Last-mile logistics would very much remain in demand.

Align with long-term structural drivers – Some structural trends going into this global health crisis would continue to dictate the trends coming out of it. Aging demographics and rising health care needs remain on an inexorable path. We favour real estate catering to this growing demand.

Essentials will always be essentials – Grocery-anchored retail catering to non-discretionary needs have long been a mainstay in the portfolios of conservative investors. If anything, this pandemic has amplified the defensive quality of these assets.

Data infrastructure play catch up –The trend towards remote communication is likely to become more deeply entrenched as a result of recent distancing measures (think work-from-home and home-based-learning). With 5G technologies at our doorsteps, the increase demand for bandwidth and data storage can only grow.

Residential for rent – Target middle-to-low end multifamily sector to be specific. Economic repercussions from COVID-19 are expected to linger long after the virus is gone, shifting residential demand from owner occupation to rent.

Non-traditional debt – As banks retreat from parts of the lending space in the flight to quality, it leaves room for nimble footed investors to deploy into some of the void left behind. We will be looking at opportunities where mezzanine pieces can now access equity-like returns. While risks may be higher, the increase returns can yet yield attractive entry points from a risk-adjusted-returns perspective.

Opportunistically Opportunistic

Last but not least, with the amount of market dislocations that have started and with more yet to come, we simply cannot resist the temptation of going through the distressed pile to see what we can find. It is not our go-to strategy, but with our connections in the real estate space, it would be a waste not to keep our eyes open for such opportunities.

On a concluding note, investors would do well to tighten risk management by exercising extra prudence in scrutinising deal underwriting assumptions, running deeper due diligence and assuming leverage cautiously in the current investment climate. In dealing with forecasts that are as wide as they are uncertain, we believe rigorous stress testing to be the best risk mitigant.

For more insights:

About RealVantage

RealVantage is a leading real estate co-investment platform, licensed and regulated by the Monetary Authority of Singapore (MAS), that allows our investors to diversify across markets, overseas properties, sectors and investment strategies.

The team at RealVantage are highly qualified professionals who brings about a multi-disciplinary vision and approach in their respective fields towards business development, management, and client satisfaction. The team is led by distinguished Board of Advisors and advisory committee who provide cross-functional and multi-disciplinary expertise to the RealVantage team ranging from real estate, corporate finance, technology, venture capital, and startups growth. The team's philosophy, core values, and technological edge help clients build a diversified and high-performing real estate investment portfolio.

Get in touch with RealVantage today to see how they can help you in your real estate investment journey.

Disclaimer: The information and/or documents contained in this article does not constitute financial advice and is meant for educational purposes. Please consult your financial advisor, accountant, and/or attorney before proceeding with any financial/real estate investments.