Understanding Buyer’s Stamp Duty

Are you looking to purchase a property in Singapore but are clueless about the buyer’s stamp duties you need to pay? Here’s some quick information.

If there is an essential thing that a property buyer in Singapore needs to know, it is the Buyer’s Stamp Duty (“BSD”). Simply put, the BSD is a tax levied on property buyers when they purchase or transfer the ownership of a property in Singapore.

When you purchase a property, you will be required to pay a BSD amount that is based on either the market value or purchase price of the property — whichever is higher. This means that even if you were to purchase a condominium of a market value of SGD2.5 million at SGD2.3 million after negotiations, the BSD you will be liable to pay will still be calculated based on the market value of SGD2.5 million instead of the actual purchase price.

BSD rates in Singapore

As a property buyer, it is imperative that you know how to calculate the BSD, in order to better gauge the costs of your property acquisition. To enhance the progressivity of the BSD regime, higher marginal BSD rates have been introduced by IRAS for higher-valued residential and non-residential properties acquired from 15 February 2023 onwards. As a quick guide, this is how the BSD is structured:

Calculating the BSD

Example of a full residential property

Using the structure above, if you were to purchase a condominium of a market value of SGD2,500,000, and the actual purchase price is SGD2,300,000, the market value will be used to calculate the amount of BSD payable, as its value is higher than the purchase price. Here are the detailed calculations:

Example of a part-residential-part-commercial property

Next would be an example of a shophouse, which is both a commercial and residential property. If you were to purchase a shophouse at a market value of SGD4,000,000, with its commercial component valued at SGD2,800,000 and its residential component valued at SGD1,200,000, your BSD payable for the property will be:

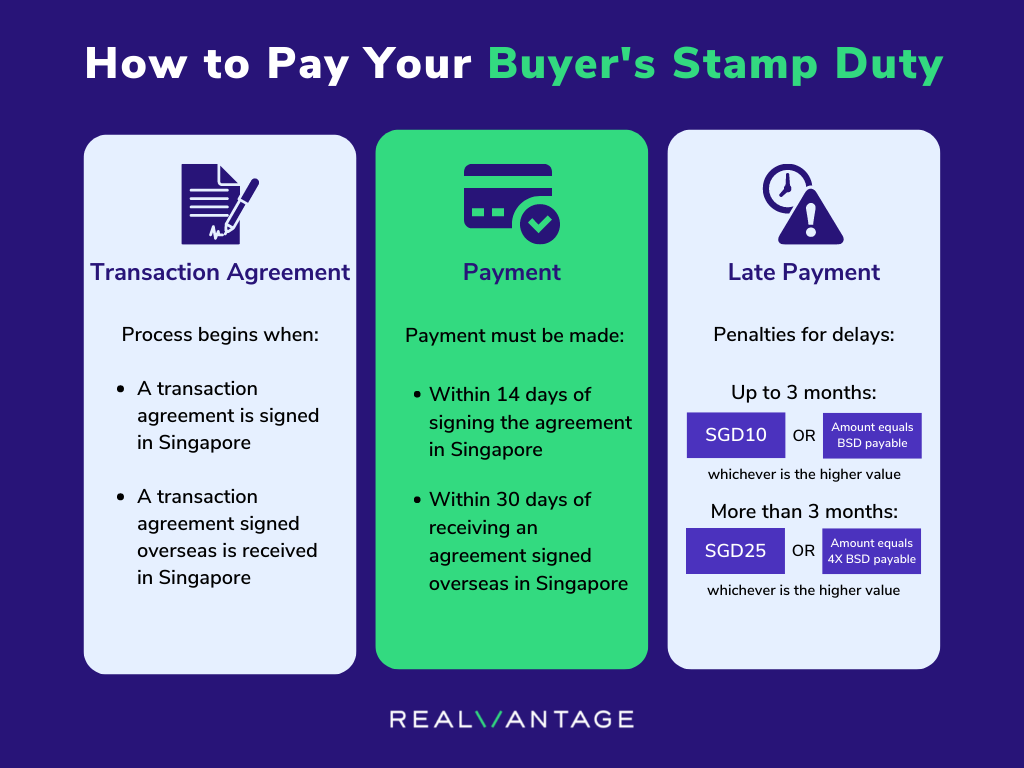

How to pay your BSD

You can pay your BSD at IRAS’s e-stamping portal or SingPost Service Bureaus. Other methods include GIRO, eNETS, Internet Banking Fund Transfer, or other methods shown on IRAS’s website.

When paying your BSD, it is important to note the timeframe for you to complete the payments.

For private property transactions that are signed in Singapore, the deadline for BSD payment is typically 14 days from the date of the agreement, namely the date when the last party signs the agreement. Where the seller grants the buyer an Option to Purchase (“OTP”), the deadline is typically 14 days from the date of the buyer’s exercise of the OTP. If the transaction was signed overseas, the deadline for BSD payment is 30 days after the agreement is received in Singapore.

Late payment for stamp duties will result in penalties amounting to the greater of SGD10 or the amount equivalent to the duty payable for late payments of up to 3 months. For late payments exceeding 3 months, a penalty amounting to the greater of SGD25 or four times the payable duty amount will be charged.

One important thing to note is that the BSD is required to be paid in full, and it cannot be paid in instalments.

BSD Frequently Asked Questions

Can I pay the BSD using my CPF savings?

You may use your Central Provident Fund (CPF) savings to pay stamp duties. However, as you would be required to pay the BSD within 14 days, you may need to pay your BSD with your personal funds first, and apply for a refund from the CPF Board (CPFB) subsequently. It is recommended by the CPFB that a property buyer apply for the stamp duty refund together with his application to use his CPF savings to purchase a property.

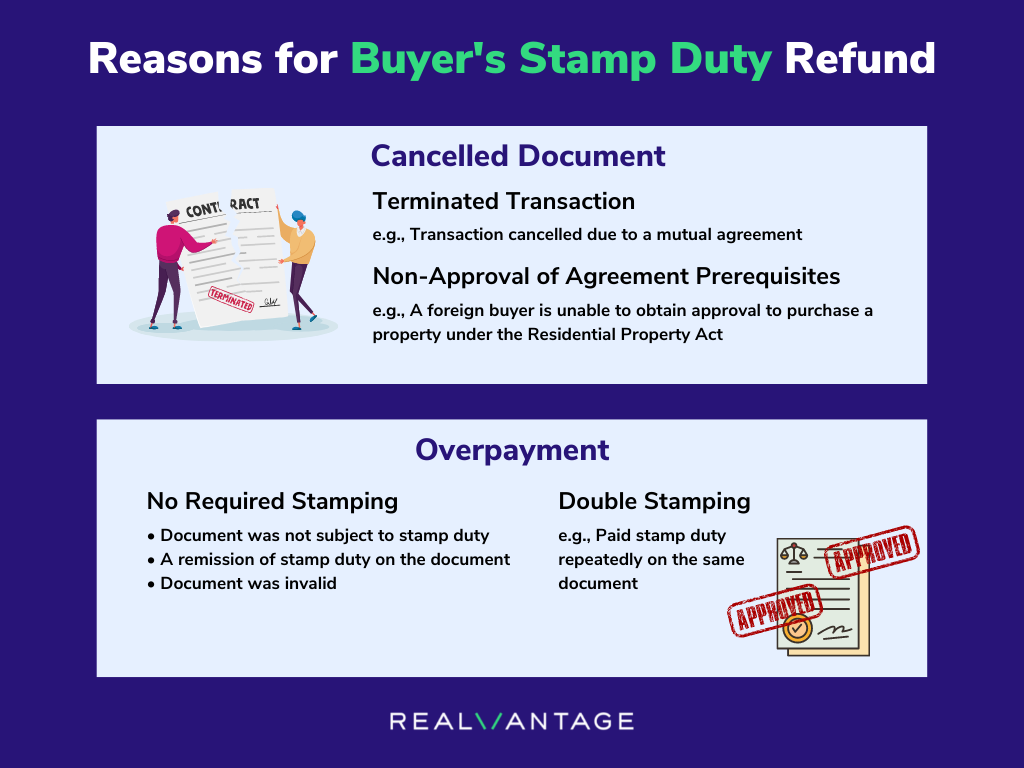

Is the BSD refundable?

Your BSD may be refunded only if specific criteria are met, and your refund claims must be applied online. For unexecuted documents, claims should be made within 6 months of the date of stamping. For executed documents, claims should be made within 6 months of the date of the document.

In which cases would there be a remission of the BSD?

These are some scenarios in which a remission of the BSD will take place:

- The property transaction is aborted

- Transfer of HDB flat ownership between family members

- Divorce proceedings

- Transfer of assets between associated entities

- Transfer of assets upon the reconstruction or merger of companies

Here’s a comprehensive list of scenarios in which a remission of stamp duties will occur and their specific criteria.

Be a well-informed property buyer

Regardless of whether you are a first-time home buyer or a seasoned real estate investor, the BSD is an important tax that you must be aware of when purchasing a property in Singapore. Knowing the BSD you will need to pay will give you a more accurate picture of the full cost of purchasing a property and help you to make more informed decisions before you commit to a real estate asset.

In addition, buyers of private residential properties are also required to pay the Additional Buyer’s Stamp Duty, which we will cover in detail in a subsequent article.

About RealVantage

RealVantage (operates as RV SG Pte. Ltd. in Singapore) is a leading real estate co-investment platform, licensed and regulated by the Monetary Authority of Singapore (MAS), that allows our investors to diversify across markets, overseas properties, sectors and investment strategies.

The team at RealVantage are highly qualified professionals who brings about a multi-disciplinary vision and approach in their respective fields towards business development, management, and client satisfaction. The team is led by distinguished Board of Advisors and advisory committee who provide cross-functional and multi-disciplinary expertise to the RealVantage team ranging from real estate, corporate finance, technology, venture capital, and startups growth. The team's philosophy, core values, and technological edge help clients build a diversified and high-performing real estate investment portfolio.

Get in touch with RealVantage today to see how they can help you in your real estate investment journey.

Disclaimer: The information and/or documents contained in this article does not constitute financial advice and is meant for educational purposes. Please consult your financial advisor, accountant, and/or attorney before proceeding with any financial/real estate investments.